How to improve your small business inventory management

By Danny Wong

When inventory management systems are working well, they enable healthy cash flow, streamline fulfilment, and reduce product spoilage. As a small business owner, it may feel like your inventory is easy to manage using manual processes because you’re deeply involved in daily operations. But it’s easy to miss key details due to information silos, delayed or inaccurate reporting, and other day-to-day distractions. And if you intend to scale up, manual systems won’t keep up with company growth.

To avoid these obstacles, many small business owners use a Point-of-Sale (POS) system to streamline their inventory management by automating tasks such as material procurement, supply monitoring, sales projection, and clearance item promotions. These systems can help simplify inventory management, reduce customer service issues, and make it easier to scale up.

Below, we’ll define inventory management, identify important inventory management techniques, detail the value of a POS system, and offer tips to improve inventory management for your business.

What is inventory management?

Inventory management involves the ordering, storing, processing, selling, and disposing of goods. Effective inventory management systems help business owners and staff optimize each part of the process.

Here are some key inventory management techniques and terms:

- Days Sales of Inventory (DSI) calculates the average turnaround time of your inventory, from ordering an item from suppliers to its sale and fulfilment.

- Economic Order Quantity (EOQ) balances bulk ordering discounts against storage capacity and costs while ensuring there is enough supply between orders to provide timely fulfilment for customers.

- Just-in-Time Management (JIT) schedules materials, manufacturing, and fulfilment to align with sales forecasts or on an as-needed basis.

- Material Requirements Planning (MRP) prioritizes having raw materials available with enough lead time to manufacture and fulfil products ahead of sales orders.

- Periodic inventory management counts inventory at scheduled intervals which can be weekly, monthly, quarterly, or annually.

- Perpetual inventory management tracks inventory in real time, noting each time an item is sold, moved, disposed of, or returned.

Inventory management: benefits and risks

Inventory management involves coordinating the many stages of moving inventory toward a sale, including ordering, storing, processing, selling, and disposing of raw materials, works in progress, and/or finished goods.

The benefits of sound inventory management

- Better planning

- Greater clarity

- On-time order fulfillment

- Reductions in dead or expired stock

- Warehousing cost savings

- Enhanced customer satisfaction

- Greater productivity

The risks of poor inventory management

- Lack of market responsiveness

- Unsold or spoiled stock

- Storage issues

- Supply chain challenges

- Dissatisfied customers and poor brand perception

Sources:

Benefits of optimized inventory management

A good inventory management system can help with:

- Sales analytics and forecasting

Accurate sales data and seasonal trends support better planning. Using sales analytics and forecasting tools, companies can plan their materials ordering, production schedules, and staffing levels accordingly. - Transfer management

Multi-location retailers can better assist each other with inventory shortages. For instance, if a sneaker store runs out of a certain shoe in a size 7, but a nearby location has available inventory in that same model and size, staff can arrange a courier to help balance the inventory between locations. - Improved customer satisfaction

When they have the right inventory available, companies can fulfil orders faster, avoid cancelled orders, and minimize out-of-stock notifications — satisfying consumer expectations.

Additionally, business owners should prioritize strategic inventory management because it can reduce:

- Confusion and shrinkage

Infrequent inventory counts may lead to a mismatch between the inventory companies believe is available and the inventory that’s actually available. This discrepancy causes fulfilment issues and frustrates customers when businesses accept orders for items that are not actually in stock. - Dead stock

Dead stock is items (generally non-perishable) that do not sell within a reasonable timeframe or become unsellable. Accurate sales data and forecasting minimize the risk of ordering excess inventory, which reduces the chances of having dead stock. - Delayed fulfilment

A timely inventory management system increases the chances that items will be available for delivery when customers place their orders. This assurance helps protect against scrambling to source products from manufacturers, which could require days, weeks, or months of lead time. - Expired stock

Expired stock is either perishable or semi-perishable, so it cannot be sold after a certain point. Sound inventory management helps businesses avoid ordering too much inventory relative to sales and reminds staff when items are at risk of spoiling. - Storage costs

Smart inventory management strategies optimize the amount of inventory on hand so a business doesn’t overpay for warehousing costs as a result of excess inventory. An inventory management e-book published by BDC shares an example in which a company selling $8 million in goods each year was able to save $100,000 annually simply by reducing excess inventory.

How can poor inventory management impact your business?

For small businesses, improper inventory management can cause headaches and drive up costs. Item shortages, excess stock, and missing inventory become common occurrences. As noted above, poor inventory management also harms brand perception and customer satisfaction.

Without a proper inventory management system, companies may run into complications with:

- Demand changes

When sales suddenly drop, owners may be unable to identify which products require heavier promotion to avoid spoilage or liquidate dead stock. When sales unexpectedly spike, businesses may not have enough materials available to meet demand or obtain clear insights into their production timelines. - Inaccurate inventory

Without accurate inventory tracking, businesses may experience spoilage, unexplainable shrinkage, and a sudden discovery of excess stock. - Supply chain challenges

Bad forecasting, a key materials shortage, or sudden changes in materials pricing can complicate cash flow, costs, and product availability.

How small business owners can improve inventory management

Engage in regular monitoring and fine-tuning.

- Use an optimized POS

Get real-time reporting on inventory counts, sales data, customer insights, revenue, and more. - Identify Key Performance Indicators (KPIs)

Set challenging and achievable goals. - Train staff

Align everyone who will participate in inventory management on best practices. - Regularly audit your inventory

Perform physical audits to protect against reporting errors, accidents, and theft and ensure accurate data. - Establish inventory minimums — and reassess regularly

Determine and assess periodic automatic replacement (PAR) levels so you aren’t surprised by seasonal or other sales trends. - Create processes for dealing with excess or dead stock

Establish guidelines for how your team defines and offloads excess stock. - Integrate sales forecasting into marketing efforts

Use data to refine ad and marketing campaigns.

Prepare for the worst

- Build strong relationships

Create rapport with suppliers and other vendors who can help during an emergency. - Identify back-ups

Find suppliers and warehouses that can help you weather an extreme spike in sales. - Consider a line of credit

Secure credit for unexpected purchases.

Sources:

- 5 Inventory Management Strategies to Improve Efficiency (2023, April 17). ProjectLine.

- Guide to Effective Store Inventory Control: Methods and Tips (2022, November 27). Indeed Canada.

- What Is Inventory Tracking? (Plus Types and Helpful Tips) (2022, September 30). Indeed Canada.

- Inventory Management Techniques (With Best Practices) (2023, March 21). Indeed Canada.

- Inventory Management – A guide for entrepreneurs. BDC.

How to improve your inventory management

Inventory management is an ongoing process. Small business owners need to actively manage their inventory, regularly conduct audits, and use the data to forecast sales and futureproof their businesses.

The following strategies can refine your inventory management processes.

Audit your inventory

Good business intelligence relies on accurate data. It’s important to audit your inventory on a regular basis — even if you automate inventory tracking. Accidents, reporting errors, and even theft can occur without oversight.

Common approaches to auditing include:

- Cycle counts or batch tracking

This strategy involves assessing batches of inventory and comparing those counts with your current records. For instance, teams can work to reconcile certain stock keeping units (SKUs), boxes, or pallets at once, then move on to the next batch. Over days or weeks, staff count through the full inventory at your stores and warehouses and cross-reference their counts with automated systems. Some businesses prefer cycle counts because this approach minimizes operational disruptions and allows for early identification of inventory issues. - Physical counts

A physical count assesses all available inventory at a given moment. This process requires a full stop to production, fulfilment, shipment, and receiving. Some business owners conduct a physical count after normal working hours to minimize operations downtime. (Of course, this strategy means you need to pay your staff overtime for after-hours work.) For companies that hold a lot of inventory, production may need to pause for several days.

Regularly review your forecasts

Small businesses can improve their inventory management strategies with better sales forecasting. Review recent and historical sales data, have conversations with your marketing and sales teams, and evaluate how the overall market is performing. Always assume you can fine-tune your forecasting.

Factors to consider include:

- Growth in your distributor network or sales pipeline

- Increases in marketing spend

- Overall category or industry growth

- Planned sales and promotions

- Seasonal changes

- Year-over-year growth

Set minimum inventory expectations

Determine and maintain periodic automatic replacement (PAR) levels for your retail stores, distribution mechanisms, and warehouses. These minimum inventory levels make sure you have enough stock on hand until the next replenishment order comes in. Reassess PAR levels throughout the year to account for seasonal trends and general sales growth.

Futureproof: prepare for what comes next

Basic inventory management accounts for current stock counts and recent sales volume. The basics are helpful for day-to-day operations, but issues can arise when unexpected situations occur. For instance, you will need contingency plans if sales spike, material costs increase, or storage space becomes unavailable.

Here are a few strategies to improve outcomes in the face of potential challenges:

- Improve vendor relations

Build rapport with your suppliers so they’ll be more likely to accommodate special requests and provide support in emergency situations. - Prepare a line of credit

Open a line of credit with your bank that will allow you to quickly access cash if you unexpectedly need to make large purchases. - Source backup suppliers and warehouses

Identify backup suppliers and warehouses to help meet extreme spikes in sales demand — before those spikes occur.

Ultimately, you want to imagine the worst-case scenarios and lay the groundwork for solutions so you’re less likely to be caught off guard.

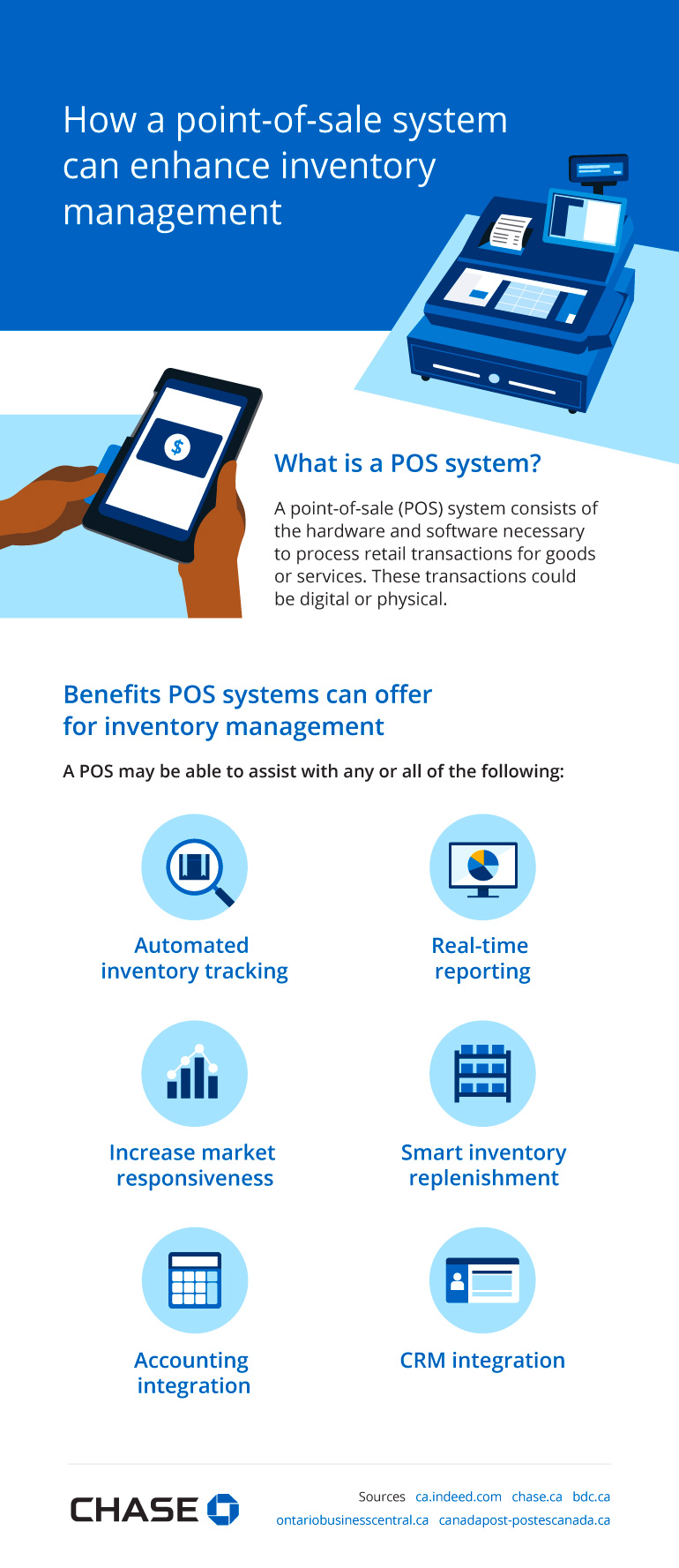

How a point-of-sale system can enhance inventory management

What is a POS system?

A point-of-sale (POS) system consists of the hardware and software necessary to process retail transactions for goods or services. These transactions could be digital or physical.

Benefits POS systems can offer for inventory management

A POS may be able to assist with any or all of the following:

- Automated inventory tracking

- Real-time reporting

- Increased market responsiveness

- Smart inventory replenishment

- Accounting integration

- CRM integration

Sources:

- What Is a Point of Sales System and How Does It Work? (2023, September 25). Indeed Canada.

- Contact Sales or Open An Account. Chase Payment Solutions Canada

- Point of Sale Systems (2023, September 15). Ontario Business Central Blog

- What is a Point of Sale? BDC.

- Choose the right point of sale (POS) system for bricks and clicks. Canada Post.

A modern point-of-sale (POS) system can simplify your inventory management processes by enabling business owners to streamline payments, track customer loyalty, and fine-tune inventory tracking.

For example, a POS system can provide:

- Automated inventory tracking

With each sale, the POS will update inventory levels and mark items as out of stock when they are sold out. Business owners benefit because items can’t be oversold, and staff save time by eliminating manual tracking. - Real-time reporting of inventory movements and sales

Quality POS systems offer real-time reporting on a variety of data points including hourly sales, daily sales, current inventory counts, monthly returns, and even past-year reports. - Enhanced sales forecasting

Using recent and historical data, you can gather useful insights from your POS to improve sales forecasting. For example, you may find that this season, certain items are more popular than last year’s favourites, which would require you to reassess the quantities in your next purchase order. - Smart inventory replenishment

You can program your POS to automatically order replenishments when inventory reaches predetermined PAR levels.

Inventory management and the customer experience

Order delays, stockouts, and other consequences of poor inventory management harm brand perception and quickly shift customer sentiment from eager and excited to anxious and frustrated. Small businesses that carefully manage their supply levels guarantee customer orders are fulfilled on time and avoid upsetting out-of-stock notifications.

Businesses can use strategic inventory management techniques to save money and time while streamlining operations and improving the customer experience. Enhance your inventory management by scheduling regular audits, developing contingency plans, reviewing sales forecasts, and establishing PAR levels. In addition, invest in the right POS system to automate and improve the way your business manages and tracks inventory.

These efforts are well worth it, because better inventory management can positively influence the customer experience and your bottom line.