Understanding your credit card processing statement: A step-by-step guide

By Amanda Reaume

Confused by your merchant processing statement? You are not alone. Many business owners get stuck trying to understand the difference between things like interchange fees, assessment fees, and wholesale rates.

Luckily, you don’t need to be the world’s foremost expert in processing to navigate the ins and outs of your merchant statement. You just need a little help mapping out what this document means for your company.

Once you get more familiar with your statement, you’ll be better equipped to understand your merchant processing expenses so you can get back to what you do best: growing your small business.

How does processing work?

When you think about processing, you likely imagine your customers swiping or tapping their cards, their transactions getting approved, and the sale swiftly ringing through. But many people and organizations are involved in the card processing journey.

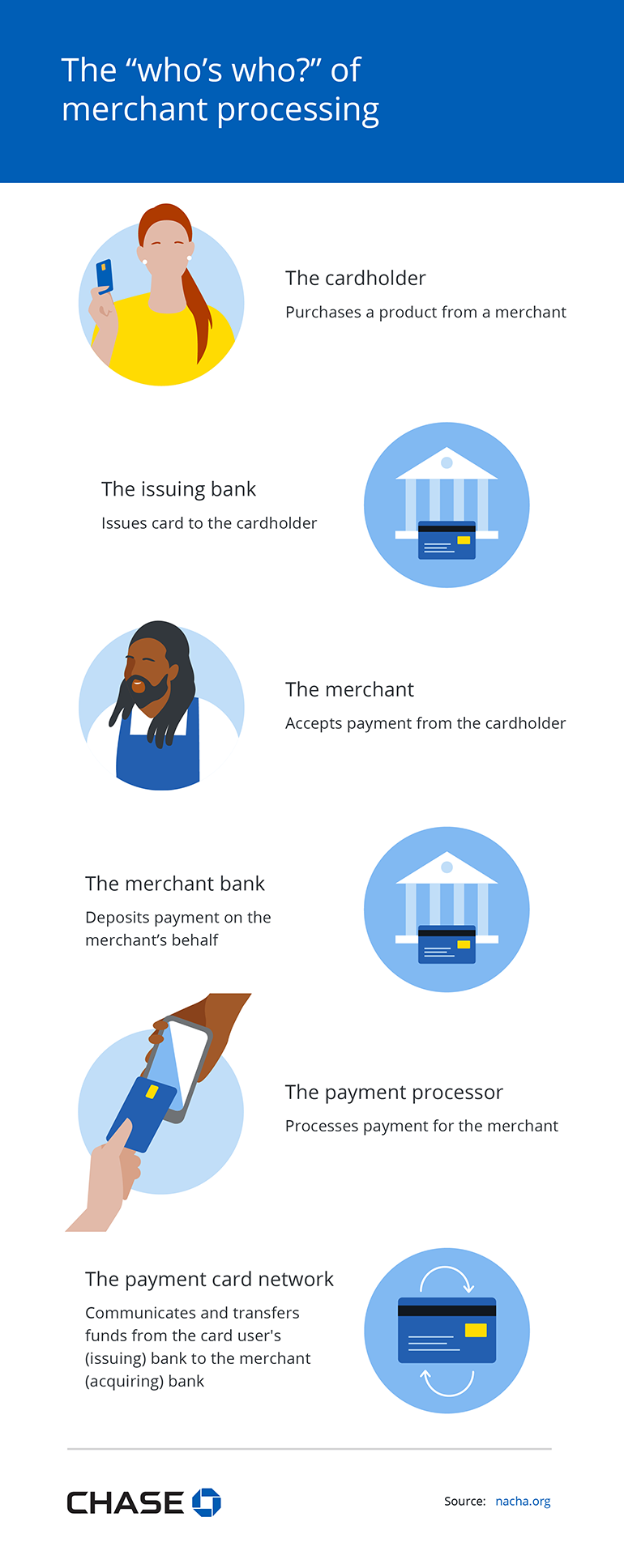

Here are all the players:

- The cardholder: the person who gets a credit or debit card from a bank

- The issuing bank: the institution that reviews card-holder applications, does a credit check for approval and issues a credit/debit card to be given to a person and/or business

- The merchant: that’s you, the business owner

- The merchant bank: the bank you use to accept deposits from credit card and debit payments

- The payment processor: the organization that processes credit and debit card payments on POS systems or via ecommerce sites. These transactions then get submitted for authorization and settlement

- The payment card networks: Large companies such as Visa®, Mastercard® and American Express® communicate and transfer the funds from the card user's (issuing) bank to the merchant (acquiring) bank

- The cardholder: Purchases a product from a merchant

- The issuing bank: Issues card to the cardholder

- The merchant: Accepts payment from the cardholder

- The merchant bank: Deposits payment on the merchant’s behalf

- The payment processor: Processes payment for the merchant

- The payment card network: Communicates and transfers funds from the card user's (issuing) bank to the merchant (acquiring) bank

Sources:

What are the steps involved in processing?

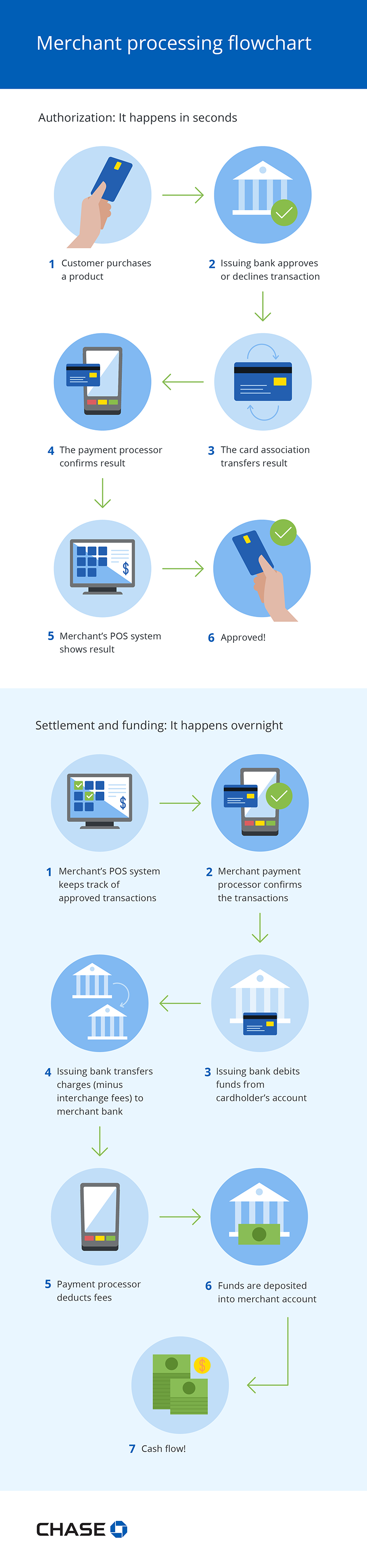

First, let’s break down the payment process. Here are the basic steps.

- Authorization

When a card is used, the point-of-sale (POS) system sends a request on the merchant’s behalf to the payment processor who submits the potential transactions to the payment card network, who then connects with the issuing bank.

The issuing bank either approves or declines the transaction and sends their response to the card association, who sends it to the payment processor and then finally to the merchant’s POS system.

It sounds complicated, but, as you know, it usually takes just seconds to get a response.

- Settlement and funding

From there, the merchant’s POS system sends approved transactions to their payment processor who ferries them along the chain until the issuing bank debits them from the cardholder’s account. The issuing bank then transfers the charges (minus the interchange fees) along the chain to the merchant bank, and the payment processor deducts their fees before the sum ends up in the merchant’s account.

That complicated process used to take several days to complete, but now many companies offer next business day funding, which assists small business’ cash flow and keeps their transactions flowing freely.

Why do you need to know the various steps involved in processing a payment, you ask? Because it helps you understand where different fees are going so your merchant statement makes more sense.

Authorization: It happens in seconds

- Customer purchases a product

- Issuing bank approves or declines transaction

- The card association transfers result

- The payment processor confirms result

- Merchant’s POS system shows result

- Approved!

Settlement and Funding: It happens overnight

- Merchant’s POS system keeps track of approved transactions

- Merchant payment processor confirms the transactions

- Issuing bank debits funds from cardholder’s account

- Issuing bank transfers charges (minus interchange fees) to merchant bank

- Payment processor deducts fees

- Funds are deposited into merchant account

- Cash flow!

How to read your merchant statement

Merchant statements itemize all your business’ payment transactions during your billing cycle and list all the fees charged on your account. That can make for some pretty long statements — yours may add up to several pages or even several dozen pages.

So, how do you decipher it? Your statement will list details like your merchant ID, your sales activity, the interchange fees for each of your transactions, any chargebacks on your account, and any other fees. It will also list the most important number: the revenue deposited into your bank after settlement and funding.

Reviewing your processing statements regularly can help you quickly and easily track your revenue and identify when your business is at its most profitable. Did you offer a promotion at the beginning of the month? You can see the results in the form of sales activity. Did you launch a new product? You’ll be able to track how well it has performed. Over time, you can use these insights to progress your business and track growth.

Key payment processing terms

Unsure what some of the payment processing terms above mean? We created a vocabulary guide to help you out!

- Billing cycle

Your business’ billing cycle could be daily, weekly, or monthly. If you set up a daily billing cycle, then your processing fees will be debited every day and you will receive a daily statement. Similarly, if you set up a weekly or monthly billing cycle, then your processing fees will be debited at the end of that term and your activity will appear on your next applicable bill.

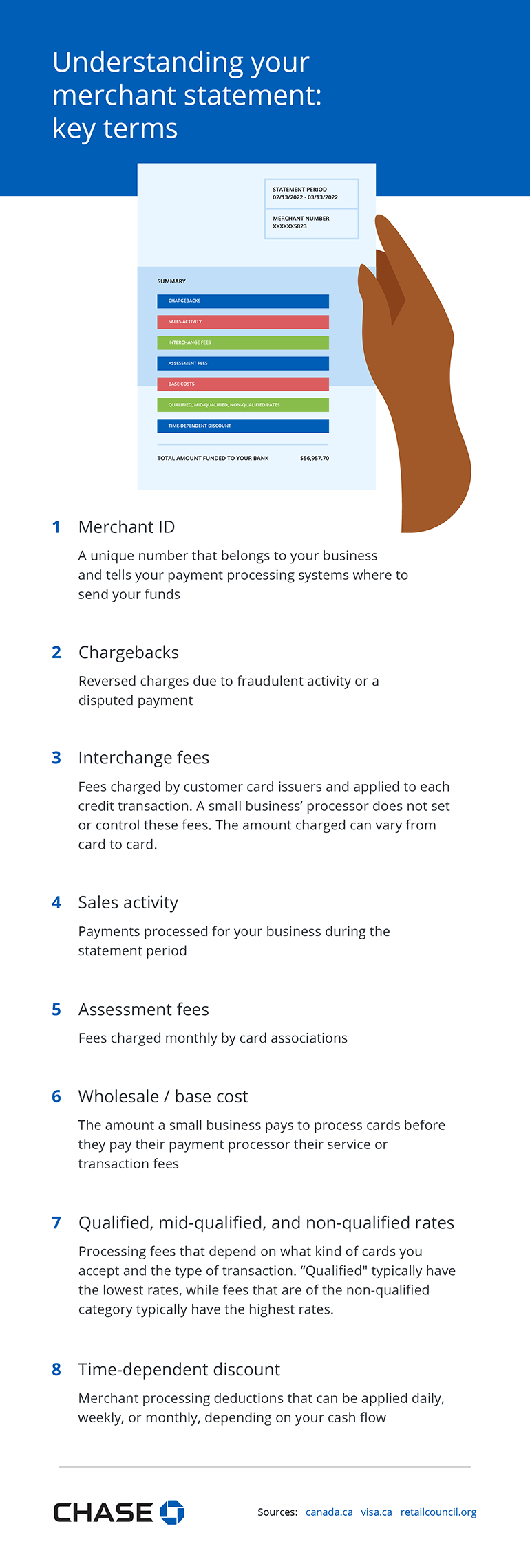

- Merchant identification number

A merchant ID is an identification number that belongs to your business and tells the payment processing systems you use where to send your funds. Merchant IDs are like bank account numbers and shouldn’t be shared widely.

- Chargebacks

Chargebacks are funds “refunded back to the cardholder.” They occur when a sale is reversed because the cardholder disputed it or because it has been connected to fraudulent activity. If the dispute is deemed valid by the credit provider, the funds are sent back to the cardholder, and your settlement account is debited. If your account has any chargebacks, they’ll typically be labelled in your statement.

- Sales activity

This is the part of a processing statement that every small business likes. It lists the number of payments processed for your business during the statement period. This amount, minus fees and other costs, is your revenue.

- Interchange fees

The issuing bank charges interchange fees, which make up the largest component of processing fees. Your payment processor does not set or control these fees, and the amount charged can vary from card to card. While the issuing bank receives these fees, the card networks set the fee structures. The government recently negotiated with Visa® and Mastercard® to lower interchange fees to 0.95% for small businesses that meet specific sales volume criteria. More than 90% of Canadian businesses will benefit from the reduction, according to the government.

- Assessment fees

Also known as brand fees, these charges are small fees (PDF) from card associations (Amex®, VISA®, Discover®, or Mastercard®). They’re typically relatively small, ranging from 0.08% to 0.15% of monthly transactions.

- Wholesale or base cost

The wholesale or base cost of your merchant processing includes the interchange fees charged by issuing banks that issue credit cards and the assessment or brand fees charged by payment card networks. This is the amount that you pay to process cards before you pay your payment processor their service or transaction fees.

- Qualified, mid-qualified, and non-qualified rates

These terms refer to the tiered pricing rubrics used by payment processors to determine how much to charge in fees for each type of card. They’re based on the hundreds of different interchange fee rates charged by issuing banks.

Different payment processors slot different kinds of cards into these buckets. Qualified transactions are charged the lowest processing fees and non-qualified transactions are charged the highest processing fees.

Generally, payment processors treat point-of-sale transactions involving a PIN as qualified cards because they’re the lowest-risk transactions. They often treat cards with certain rewards programs as mid-qualified cards because these purchases carry higher interchange fees. And they typically treat remote transactions as non-qualified cards because they come with the greatest risk of fraud.

- Daily discount versus monthly discount

Do you have your payment processing fees deducted from your account daily or monthly? What’s best for you depends on your business. Some business owners prefer daily discounts so they know how much cash they have on hand at any time, while others prefer monthly discounts to help with cash flow and reconciliation. Contact us today and a Chase representative can help you find what works best for you and your business.

- Merchant ID: A unique number that belongs to your business and tells your payment processing systems where to send your funds

- Chargebacks: Reversed charges due to fraudulent activity or a disputed payment

- Interchange fees: Fees charged by customer card issuers and applied to each credit transaction. A small business’ processor does not set or control these fees. The amount charged can vary from card to card.

- Sales activity: Payments processed for your business during the statement period.

- Assessment fees: Fees charged monthly by card associations

- Wholesale / base cost: The amount a small business pays to process cards before they pay their payment processor their service or transaction fees

- Qualified, mid-qualified, and non-qualified rates: Processing fees that depend on what kind of cards you accept and the type of transaction. “Qualified" typically have the lowest rates, while fees that are of the non-qualified category typically have the highest rates.

- Time-dependent discount: Merchant processing deductions that can be applied daily, weekly, or monthly, depending on your cash flow.

Sources:

Calculate and track your effective rate

Want to do a bit of math that will help you better understand your business?

Calculating your effective rate allows you to track how your processing fees vary month over month and how much credit processing actually costs your business.

Your effective rate will give you a better idea of the true cost of your processing. All you need is:

- Your total sales activity (TSA)

- The total amount of fees you were charged (TF)

Now, divide your total fees by your total sales activity: TF/TSA = Your Effective Rate

Need an example?

Let’s say you brought in $10,000 in sales and added up $500 in fees on your processing statement. Your effective rate equation would look like this:

$500/$10,000= 0.05 or 5%

If your effective rate seems high, don’t worry. Remember, it’s a cumulative rate that boils down all of your processing fees into a single number. Be sure to do some research and find out if your effective rate is the right one for you.

Total Fees Charged/Total Sales Activity = Effective Rate

Example:

$500/$10,000 = 0.05

or 5% Effective Rate

- If your business is getting lost in a sea of processing fees, calculating your effective rate is a simple way to see the true cost of merchant processing.

- Use your effective rate to track how much card processing costs your business, month over month.

- Knowing how much you’re paying in processing fees will help you better understand your profit margins, manage expenses, and grow your business.

Review your statements regularly

Now that you have the tools to fully comprehend your processing statements, you should be reviewing these documents regularly. Regular reviews of your statements can help you keep on top of chargebacks and monitor fees. Often, these issues can be on an accelerated timeline. For instance, if you want to dispute chargebacks, you typically only have a couple weeks to do so. If you notice a mistake in your statement, it’s important to tell your payment processor immediately.

Knowing how much you’re paying in processing fees will also help you better understand your profit margins. In turn, you can set prices that offset the cost of merchant processing, properly manage expenses, and grow your business.

Still have questions?

You’re off to a great start using your merchant statement to gain insights into your business. But if you’re still confused, your payment processing provider is always there to help.

As a small business owner, you’re always on the clock and so is your credit processor. If you can’t call your processor directly, you can always get started online.